A manageable monthly payment is one of the the top priorities for most buyers when considering a mortgage. That payment is made up of not only the principal and interest of the loan, but also home owner’s insurance, property taxes and HOA dues if you’re buying a condo. In addition, there’s monthly mortgage insurance to consider if you’re not putting 20% down.

The majority of first time buyers last year purchased with 6% down or less (according to the National Association of Realtors). So were they all stuck with monthly mortgage insurance? Not necessarily! Here’s a breakdown of few mortgage insurance options –

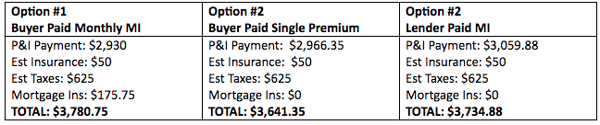

- Buyer Paid Monthly Mortgage Insurance – this is the version most consumers are familiar with. It is the traditional monthly mortgage insurance paid by the buyer, and added to your monthly payment. This usually results in the HIGHEST total monthly payment.

- Buyer Paid Single Premium (Financed) - in this version there is no monthly mortgage insurance payment. Instead, it is put into a lump sum and financed into your loan. Even though your loan amount will be higher, you are paying the mortgage insurance premium over the life of your loan. This usually results in the lowest payment.

- Lender Paid Mortgage Insurance – in this option, you have no monthly mortgage insurance or added premium that is financed into your loan. The lender is able to remove your mortgage insurance with less than 20% down, by increasing the interest rate.

Here’s the difference between each option at a $600,000 purchase price with 5% down –

These are just three of the many options available. All of them will vary based on your credit score and the amount of down payment you have, but be sure to explore your mortgage insurance options with a lender – you aren’t stuck with traditional mortgage insurance if you have less than 20% down!

Note: Not all buyers may qualify for the options stated above, please consult your loan officer to find out if you can avoid mortgage insurance.

This post is a guest post by Sean Aguirre of American Pacific Mortgage. Learn more about Sean and contact him here.